Europe’s Uranium Puzzle

- Europe Focus Group

- Apr 21

- 21 min read

An overview of the EU uranium supply

Written by Andrea Ceciliani and Kaspar Sõukand

Nuclear energy currently stands out as a significant component of the European Union’s electricity mix, providing around one-quarter of the bloc’s total electrical output and roughly one-third of its low-carbon power. Traditional large-scale nuclear reactors are primarily categorized by the specific cooling systems and moderators they use to manage the fission process, ranging from designs that use standard light water to those utilizing specialized heavy water or steam; twelve EU member states currently operate nuclear power plants, with technologically diverse reactor fleets: France predominantly uses domestically-developed pressurized water reactors (PWRs) and has the largest installed base, generating more than half of the EU’s nuclear-generated electricity; Other countries (among which Spain, Sweden, Finland, Belgium, Hungary, Slovakia, Czechia, Romania, Bulgaria, Slovenia, and the Netherlands) operate various combinations of PWRs, boiling water reactors (BWRs), and in Romania’s case, Canadian-designed pressurized heavy water reactors (PHWRs). Germany phased out its nuclear fleet in 2023, ending decades of operation, in a controversial decision which has led to economic and environmental setbacks.

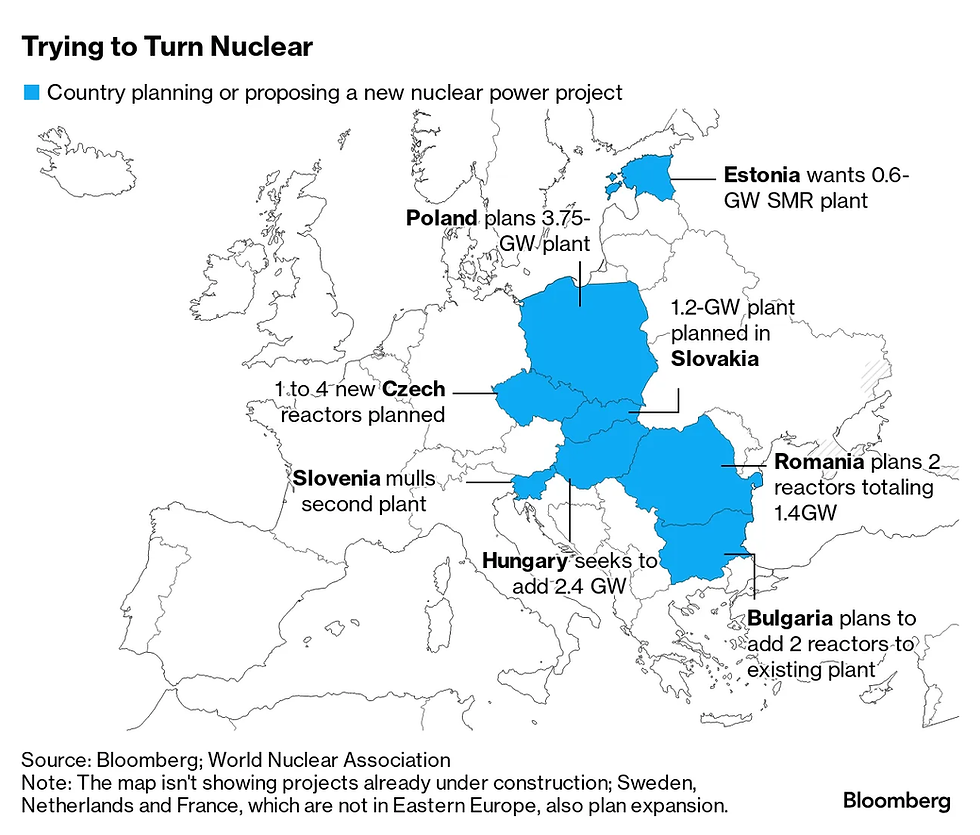

In addition, Poland is actively planning its first commercial reactors, while others are extending the lifetimes of existing units or exploring advanced reactor technologies like Small Modular Reactors (SMRs). Overall, the majority of the EU member states which do not yet possess an active nuclear power plant, are showing a growing interest in the development of a national nuclear industry.

With nuclear energy’s role expanding across the continent, the focus now shifts to the security of the fuel that powers it. This article analyzes the numbers, opportunities and obstacles within the European nuclear fuel supply chain in an era of geopolitical uncertainty and technological growth.

The nuclear fuel cycle

Firstly, it is important to briefly contextualize the fuel cycle, as it is necessary for understanding the nature of nuclear fuel demand. The nuclear fuel cycle encompasses the full sequence of industrial and technological processes required to transform uranium ore into usable reactor fuel and to manage the resulting radioactive waste after irradiation. Conventionally, the cycle is divided into three major phases: the front end, power generation, and the back end. The front end begins with uranium mining and milling, during which ore is processed into uranium concentrate, commonly known as “yellowcake.” This concentrate is then chemically converted into uranium hexafluoride (UF₆), a form suitable for isotopic enrichment. Enrichment increases the concentration of the fissile isotope uranium-235 from its natural level of roughly 0.7% to the levels required by most commercial reactors, typically between 3% and 5%. The enriched uranium is subsequently fabricated into ceramic pellets, inserted into metal fuel rods, and assembled into fuel bundles for reactor use.

During power generation, these assemblies are loaded into reactor cores where controlled fission reactions produce heat that is converted into electricity. Over time, fissile material is consumed and fission products accumulate, reducing fuel efficiency, therefore requiring regular refueling cycles every 12 to 24 months. The back end of the cycle begins once fuel is discharged. Spent fuel may be stored, directly disposed of, or chemically reprocessed to recover unused uranium and plutonium for recycling, depending on national policy and technological capacity.

There are two primary fuel cycle models: open (once-through) and closed (reprocessing). In an open cycle, spent fuel is treated as waste after irradiation and stored for geological disposal. While technically simpler and requiring less infrastructure, this method consumes more uranium and generates higher volumes of high-level waste. Conversely, a closed cycle reprocesses spent fuel to extract uranium and plutonium, typically recycling them into mixed oxide (MOX) fuel. This increases resource efficiency and reduces the volume and radiotoxicity of final waste. While advanced concepts like fast breeder or thorium cycles exist, they are not yet commercially deployed within the EU.

Within the European Union, national approaches to the fuel cycle vary considerably according to historical policy choices, reactor technologies, and industrial capabilities. France represents the most developed example of a closed fuel cycle. Through the integrated operations of Orano, uranium is converted, enriched, fabricated, and ultimately reprocessed domestically. Spent fuel from French reactors is routinely sent to the La Hague reprocessing facility, where plutonium and residual uranium are separated and recycled into MOX fuel. This strategy reduces natural uranium requirements, strengthens energy independence, and forms a central pillar of French nuclear policy. Belgium and the Netherlands have also incorporated elements of recycling into their systems, with both countries licensing and occasionally using MOX fuel, although they rely on foreign facilities for reprocessing. Most other EU Member States employ predominantly open or partially open cycles.

The functioning of Europe’s fuel cycle depends on a complex ecosystem of specialized firms that operate across each stage of the process. A critical industrial actor within this ecosystem is the aforementioned Orano, a major European nuclear fuel cycle company. Orano supplies advanced fuel technologies to utilities in the EU and beyond, thereby supporting reactor operations and contributing to the bloc’s fuel security. Orano’s activities align with broader policy goals to reinforce European supply chains and reduce reliance on non-EU sources for essential nuclear inputs. Besides Orano’s vertically integrated operations, enrichment services are heavily supported by Urenco, a multinational consortium with centrifuge enrichment facilities in Germany, the Netherlands, and the United Kingdom that supplies enriched uranium to utilities across Europe and globally. Fuel fabrication and reactor-specific assembly design are also provided by Westinghouse Electric Company, which has expanded its presence in European markets, particularly by developing alternative fuel for (Russian) VVER reactors to support diversification strategies. Additional fabrication capacity is supplied by Framatome, including its subsidiary FBFC, which produces assemblies for numerous European light-water reactors. Historically, several Member States have also relied on services from TVEL and TENEX, subsidiaries of Russia’s state nuclear conglomerate Rosatom, particularly for VVER-compatible fuel and enrichment. Although these suppliers remain technically significant, geopolitical developments have accelerated European efforts to diversify toward domestic or allied alternatives.

Taken together, it is possible to observe that the European fuel cycle is not a single unified system, but rather a network of interconnected national infrastructures linked by shared enrichment, fabrication, and regulatory frameworks coordinated through Euratom institutions. The combination of domestic industrial champions and international suppliers ensures operational continuity, yet additionally raises strategic questions about supply security and autonomy. Consequently, a question emerges: how resilient is the European uranium supply?

The European Union's uranium supply needs

The scale of uranium demand in the European Union is directly determined by the size of its operating reactor fleet. With roughly 98 reactors and about 96 GWe of installed capacity, nuclear power plants consume significant volumes of fresh fuel each year to sustain baseload generation. According to the Euratom Supply Agency (ESA), EU utilities loaded approximately 1,761 tonnes of fabricated fuel in 2024, which required about 12,120 tonnes of natural uranium equivalent (tU) as feed material. This figure provides the best aggregate estimate of annual uranium requirements for the EU-27 and establishes the bloc as one of the world’s largest civilian uranium consumers.

Fuel fabrication requirements also reveal the technical characteristics of European reactors. ESA reports that the 2024 reloads were enriched using 9.17 million separative work units (SWU) to an average enrichment of 4.15% U-235, with tails assays around 0.20%. These values are consistent with the light-water reactor (LWR) technology that dominates the EU fleet. Because enrichment levels and tails assays strongly influence how much natural uranium is required, improvements in enrichment efficiency or tails optimization can reduce raw uranium demand even when electricity output remains constant.

Uranium needs are unevenly distributed across member states, largely reflecting differences in installed capacity. France alone accounts for more than half of EU nuclear generation and therefore dominates uranium consumption, requiring roughly 8,200-8,300 tonnes of uranium annually. Spain, Sweden, Czechia, Finland, Slovakia, and Belgium follow, each consuming several hundred tonnes per year. Finally, smaller nuclear states such as Slovenia and the Netherlands require less than 150 tonnes annually. However, because procurement and stockpiling remain strictly national competencies, these countries (rather than any multilateral organization) independently determine their own purchasing volumes and strategic reserve levels based on their specific energy security needs.

The following table provides a comprehensive snapshot of the nuclear power landscape across Europe as of 2026. It highlights the numbers of active generation capacity, future construction plans for nuclear plants, and the raw materials required to sustain them. Countries without operating reactors, such as Poland, currently have no consumption but will add to demand once planned reactors enter service. These numbers highlight both the concentration of demand and the potential for future growth as new-build projects materialize.

TThe type of fuel required in each country depends primarily on reactor design. As previously mentioned, most EU states operate light-water reactors, either pressurized water reactors (PWRs) or boiling water reactors (BWRs), that use low-enriched uranium (LEU) fuel enriched to roughly 3-5%. France, Belgium, Spain, Sweden, Finland, and the Netherlands predominantly use Western-designed PWR or BWR assemblies. Central and Eastern European countries operate VVER reactors, a Russian-designed variant of the PWR concept that requires different fuel geometries and historically relied on specialized suppliers, although technically still based on LEU. Romania is distinct in operating CANDU heavy-water reactors that can use unenriched uranium, eliminating enrichment requirements but increasing natural uranium consumption per unit of electricity generated.

Beyond differences in reactor types, the EU maintains substantial industrial capacity across the front end of the fuel cycle. Conversion, enrichment, and fuel fabrication are largely provided domestically by companies such as Orano and Urenco, which together supply most enrichment services within Europe. This internal capability reduces reliance on external enrichment markets and stabilizes procurement costs. It further means that the EU’s uranium needs are not simply a matter of mining supply but depend on integrated processing capacity and long-term contracting strategies.

Uranium demand exhibits relative stability over time compared with fossil fuels. As previously mentioned, the fact that reactors refuel on predictable 12-24 month cycles means that utilities typically maintain multi-year inventories. Particularly, Euratom has noted that stockpiles often cover at least one to three years of consumption. Consequently, the EU’s annual requirement of roughly 12-14 thousand tonnes U can be considered structurally steady rather than highly volatile. This predictability is strategically important, allowing long-term supply planning and buffering short-term market disruptions, a feature that differentiates nuclear fuel from gas or oil markets.

From home to abroad: evolution of EU’s uranium supply

ETo understand the reliance of the European Union on external uranium suppliers we can analyse the historical role of the Soviet Union as the first producer of nuclear energy in Europe. In 1945 the Soviet Union faced a great challenge, having just been instrumental in winning World War II and taking control over most of Eastern Europe they now saw their previous allies as new adversaries. The United States had just been able to create and use the world’s first nuclear weapons, demonstrating new, and more devastating military capabilities. The Soviet Union’s own efforts to construct a nuclear weapon were, however, moving slowly as pro-American governments controlled the largest uranium mines located in Canada, South Africa and the Congo, depriving the USSR of necessary resources. Cut off from foreign sources and with the territory of the USSR mostly unsurveyed, the Soviet nuclear weapons program made use of territories in their sphere of influence which had been better surveyed for uranium deposits. Under the cover of Wismut mining company the Soviet Union sent 200 000 prisoners to work in East Germany, raising it into the fourth biggest uranium producer in a matter of years. The supply of uranium from East Germany was complemented by provisions by other Eastern European satellite states, and was processed in the Estonian SSR. Using labour from the GULAG prison camp system, as well as through its political prioritisation within the country's economic policy, the USSR became the foremost producer of nuclear fuel during the 1950s.

In the first decades of nuclear energy development in Europe the mines found and developed in Europe were the primary source of uranium. The Soviet Union continued to receive the majority of its uranium from Eastern European satellite states, meanwhile France expanded uranium mining in the regions of Limousin and Vendée. This began to change during the 1960s and 1970s. Particularly, the focus of uranium mining in the USSR shifted to the central Asian republics with mines opened in Kyrgyzstan, Tajikistan and especially Kazakhstan. Simultaneously, France started exploiting and became reliant on Nigerien uranium. Yet mining in Europe continued even as its importance in the global supply decreased. The end of the Cold War signalled the end for continued uranium production in Europe, due to its increasing costs and a lack of available financial support. Most formerly socialist states in Central and Eastern Europe closed their uranium mining operations by 1992. Although limited uranium mining operations continued in Czechia and Romania, both states ultimately opted for their closure after a decrease in global uranium prices during the 2010s.

Therefore, when the Russian invasion of Ukraine began in 2022 the European Union had little domestic uranium production. In 2021 the European Union imported 24% of its uranium from Niger, 23% from Kazakhstan, 20% from Russia, 15.5% from Australia and 14% from Canada; only 0.17% of uranium came from the EU itself. While European raw uranium imports came from multiple source countries, the outbreak of the Russo-Ukrainian war exposed the reliance upward in the fuel cycle and how Eastern European states relied primarily on Russian uranium. It also raised questions for French strategy, as the French nuclear energy program had become largely reliant on Nigerien uranium supply.

Despite this, the shift toward more resilient nuclear supply chains has been slow. Russian uranium was excluded from sanctions by the European Union.In fact imports of Russian uranium increased as European countries went through a stockpiling frenzy in 2023. While Russia has lost some of its share in the uranium market, the country which saw the largest decrease in uranium exports to the EU since 2021 has undoubtedly been Niger, which saw its share in the EU market drop from 27% in 2022 to 8% in 2024. As political conflicts continue between the military government in Niger and the European Union, this figure may decrease even further in the upcoming years. Kazakhstan has kept its position as the second most important uranium exporter for the EU while China and Australia have become increasingly important. However, the country which has experienced the largest increase in its market share as a result of global geopolitical disruptions has been Canada, with its share as part of the EU’s uranium supply rising from 14% to 33% between 2021 and 2024.

A more detailed understanding of how dependencies on nuclear fuel and uranium suppliers have led to disruptions can be offered by looking at the consequences of the Russo-Ukrainian war and Sahel crisis.

Now we will look more in detail about the current existing dependencies in the EU's nuclear supply chain related to the ongoing conflict in Ukraine.

The consequences of the Russo-Ukrainian war

Since the Cold War, both Russia and Ukraine have been significant nuclear energy producers as well as being important uranium exporters globally. Before 2022 Russia and Ukraine contributed 5.43% and 2.21% of the global uranium mining respectively, however, they remain net importers of raw uranium.

Russia specifically played an important role in the European Union’s uranium supply before the Russian invasion of Ukraine, with Russian uranium constituting almost 1/5 of the all uranium imports. While Russian gas and oil are relatively more important within the context of the European Union’s energy policy, Russia’s role as both a major domestic producer of uranium, and an increasingly influential player in Niger made European nuclear energy particularly exposed to Russian political decisions. This issue is further exacerbated by the reliance of the European nuclear industry on Russian products in the earlier phases of the fuel cycle. While Europe has increasingly diminished the direct usage of Russian nuclear products, a significant portion of uranium remains mined, converted or enriched in Russia.

Its importance in fuel manufacturing is even more significant. Soviet or Russian produced VVER reactors are still used in Bulgaria, Czechia, Finland, Hungary, Slovakia as well as in multiple European countries outside of the EU. Russia has historically been the sole producer of fuel for VVER reactors. Recently, the U.S. firm Westinghouse began the production of fuel for VVER reactors, with the French company, Framatome, in the process of starting its own production.

However, Framatome’s efforts to create a European substitute suffer from structural limitations, which may lessen their significance in the pursuit of European strategic autonomy in the nuclear sector. The production of nuclear fuel for VVER reactors will be a joint Franco-Russian project, with Rosatom supplying specific components, fuel designs and licenses. While this would curb imports of Russian nuclear industry goods which between 2022 and 2023 was estimated at around 900 million euros, it would still let Russia generate profits from its nuclear industry and give them the ability to bypass attempts at decoupling undertaken by the European Union.

Therefore, despite recent attempts at restricting Russian market access to European nuclear fuel and uranium markets through the development of substitutes, Russia’s role as the main provider of nuclear goods for VVER reactors limits their effectiveness, and constrains the possibility for sanctions. The European Union currently has around three years worth of uranium in its reserves, yet despite starting the APIS and SAVE projects to design domestic VVER fuel and shifting its supply chains towards countries like Canada and Kazakhstan a full decoupling from Russia as a supplier looks unlikely in the medium-term.

The Sahel crisis

Since the start of France's civil nuclear program, it has relied heavily on Niger as a uranium supplier. Despite obtaining independence in 1960, and severe political instability, including five coups d'état and four periods of military rule, French mining companies retained ownership of local uranium mines. France’s involvement in Niger was led by Orano, who held an 11% share in global uranium production. The company is deeply linked to the French state, with the latter holding a 90% share in Orano. The continued French ownership of uranium mines, along with other factors linked to the legacy of colonialism, has been a source of anti-French political sentiments in Niger. In July 2023, Niger experienced a coup d’etat which resulted in the formation of a military junta with a markedly anti-western political orientation, as demonstrated by their decision to expel French and American forces, stationed as part of anti-terrorism operations in the Sahel, from the country. The new regime quickly turned its attention towards Somaïr, the main mining company of Niger, which was firmly under Orano’s control. In 2024, Orano lost operational control over the uranium mines in Niger and in June 2025 Niger announced its plan to completely nationalize Somaïr.

Eviction of French mining company for Niger has left a door open for new countries to take its place. Russia has been thought to have played a significant role in the 2023 coup, exemplified by pro-coup protestors taking to the streets with Niger and Russian flags during the coup. In 2024, the military instructors from Russia’s Africa Corps were deployed to Niger and multiple cooperation agreements were signed between these countries. However, the complicated relations with ECOWAS has left the shipment of uranium to Russia stuck on the Niger border. The China National Nuclear Corporation has also been planning to restart its uranium mine in Azelik amidst a new push to the African nuclear energy market. Currently, however, Niger has lost its importance as a global uranium producer, being unable to sell its stockpiles after severing ties with France.

This erosion of French influence in West Africa serves as a catalyst for a broader re-evaluation of Europe’s nuclear future. The transition away from unreliable external suppliers of raw uranium is now converging with a technological leap toward Small Modular Reactors, a shift that promises greater autonomy but introduces new, complex challenges in the fuel enrichment market.

HALEU and SMRs development

Particularly interesting in the context of building up a resilient nuclear fuel supply chain was a recent European Parliamentary Research Service briefing written by Vasco Guedes Ferreira, titled “Strategic autonomy and the future of nuclear energy in the EU”. In this paper, the author discusses the outlook for nuclear energy in the EU and analyses the transition from traditional, large-scale generation toward a more flexible and technologically advanced open strategic autonomy. While nuclear energy currently generates 23% of the EU's electricity, the sector faces a critical juncture: 83% of existing reactors are over 30 years old. To meet the legally binding target of net-zero emissions by 2050, the European Commission’s modeling suggests nuclear power will have to play a significant role, particularly in the electrification of the economy and the move away from Russian fossil fuels.

A new strategy that could enhance the role of nuclear energy is the deployment of SMRs, with commercial viability anticipated by the early 2030s. Unlike conventional gigawatt-scale plants, SMRs (usually up to 300 MWe) and microreactors (1-20 MWe) offer plug-and-play versatility. They are designed for factory assembly and transport, making them ideal for replacing aging coal plants or powering remote areas. Beyond electricity, they can serve an important role with their cogeneration potential-providing high-temperature heat for district heating, desalination, and the chemical production of hydrogen. To accelerate this, the EU has launched a European Industrial Alliance on SMRs, aiming to harmonize standards and streamline the licensing of all the different designs currently in development globally.

The successful rollout of these advanced reactors depends heavily on a specialized fuel called High-Assay Low-Enriched Uranium (HALEU), which is essential for many "Generation IV" and advanced reactor designs (although not all SMRs use it). While conventional reactors use fuel enriched to less than 5% (LEU), HALEU is enriched to between 5% and 20%. This higher concentration allows for smaller reactor cores, longer intervals between refueling (up to 3 years or more), and significantly reduced waste volumes. However, a major geopolitical risk exists: Russia’s Rosatom (via its subsidiary Tenex) is currently the world’s only commercial supplier of HALEU. This creates a policy dilemma wherein the technology intended to provide energy security currently relies on a single, unreliable external supplier.

To secure its autonomy, the EU, through the Euratom Supply Agency, is working to build a domestic HALEU supply chain. While European leaders like Orano and Urenco possess the technical enrichment capabilities, they face an investment gap. With commercial production in the EU currently holding a demand for HALEU being only 1 tonne, while to make the technology commercially viable demand must increase to between 3 to 8 tonnes To bridge this, the EU is looking toward the U.S. and UK models to stimulate private investment until the SMR market matures.

The future of nuclear energy in the EU

The global energy crisis which started in 2021 and escalated following the Russian invasion of Ukraine has led to the re-emerging of nuclear power as a strategic pillar of European energy security. After years of political division the European Union is once again moving towards increased nuclear energy usage. Countries such as Poland and the Czech Republic are expanding programs, while others are reconsidering earlier phase-out plans. As the European Union focuses more and more on internalizing its energy production and switches to renewable energy, the increased importance of nuclear energy production could be an important component of achieving these goals. However, while increasing its nuclear energy production Europe should also increase its own capacity to provide for this industry to not to fall deeper into another, more complicated dependency.

While increasing the production of inputs for Europe’s nuclear industry is challenging, the European Union has that capacity. Europe is not only one of the biggest nuclear energy producers but also has a significant uranium enrichment and fuel production capacity. It fields a highly developed research and industrial base with many firms engaged in producing necessary materials and parts for the nuclear supply chain.

After three years of no uranium mining in the European Union, in 2024 Finland began recovering uranium as a by-product of zinc and nickel production at Sotkamo mine. Sweden, who has some of the biggest uranium deposits in Europe, announced an end to an 8-year old ban on mining uranium in January of 2026, together with promising to ramp up nuclear energy production.

European capacity to convert, enrich and manufacture fuel is already more than enough, but concerns about price and reliance on Russian reactors has limited the ability to move toward a domestic supply chain. In the coming years this production capacity is likely to increase with multiple projects led by Orano and the European Union planned. Scaling up fuel production is definitely in the interests of the EU as the next decade will see an unprecedented growth in the internal demand. The energy crisis and green transition have prompted a new wave of nuclear power plant construction in Europe. Western European countries such as Sweden, France and Netherlands plan on expanding their nuclear energy production, while, a number of Eastern European states, including Romania, Bulgaria, Czech, Slovakia, Hungary and Slovenia plan to expand current capabilities, with Estonia, Poland and Serbia beginning to develop plans for the creation of domestic nuclear energy projects.

Leveraging its wide range of expertise and increasing fuel production, Europe could re-establish its importance as a provider of nuclear energy-related resources to the world. Since the fall of the Soviet Union, Russia has done exactly that through using Rosatom as a branch of nuclear energy diplomacy in Eastern Europe, Africa and Asia. While Russia has been successful in reducing Orano’s control over uranium mining in Niger and used its primary position as a supplier of VVER nuclear fuel to pressure European countries to avoid sanctioning Rosatom, the dependency cuts both ways. European countries have already started to consolidate their nuclear supply chains and have begun to move away from Russian supplies. Due to the much larger market and industrial capacity of the European Union, in the long run this will likely lead to disastrous effects for Rosatom.

The long term supply of raw uranium remains an important consideration for the European Union. It is unlikely that the EU will ever produce enough domestic uranium to fulfil its internal demand. Instead, increased closeness with Canada as well as the recent trade deals negotiated with India, China and Mercosur are the most realistic avenues toward securing a consistent supply of uranium for the future. Brazil, especially, is on its way to establishing itself on the global uranium market, with large uranium deposits and burgeoning domestic enrichment capabilities. Kazakhstan’s uranium industry has always been deeply interconnected with Russia but in light of deteriorating relations since 2022, the possibility of EU-Kazakhstani cooperation on nuclear energy related topics appears to be increasingly likely. Supporting Kazakhstan’s uranium industry and tying it with Europe would greatly limit the power of Rosatom in Asia and the power of the Russian state in Kazakhstan.

In conclusion, the grand vision of a nuclear-powered Europe depends entirely on the resilience of the fuel supply chain that feeds it. Europe can no longer afford to be a passive consumer and ensuring energy security in an era of turbulence requires an aggressive commitment to domestic capacity and the foresight to secure new, reliable alliances. The foundation is laid, but the window of opportunity is narrow; failure to act on its quest for autonomy today will leave Europe paying an ever-increasing price for yet another trap of foreign reliance.

Bibliography

Adombila, M. A. (2025, December 1). France's Orano says uranium convoy from seized Niger mine poses safety risks. Reuters. https://www.reuters.com/world/africa/frances-orano-says-uranium-convoy-seized-niger-mine-poses-safety-risks-2025-12-01/

Al Jazeera. (2025, June 20). Niger to nationalise uranium mine operated by French state-affiliated firm. https://www.aljazeera.com/news/2025/6/20/niger-nationalises-uranium-mine-as-spat-with-french-nuclear-giant-worsens

Anca Benera, Arnold Estefán; The Missing Mountain. ARTMargins 2025; 14 (2): 113–128. doi: https://doi.org/10.1162/artm_a_00416

APIS Project. (2024, January 29). VVERs in Europe. https://apis-project.eu/vvers-in-europe/

Bele, J. (2021, February 28). The legacy of the involvement of the Democratic Republic of the Congo in the bombs dropped on Hiroshima and Nagasaki. MIT Faculty Newsletter. https://fnl.mit.edu/january-february-2021/the-legacy-of-the-involvement-of-the-democratic-republic-of-the-congo-in-the-bombs-dropped-on-hiroshima-and-nagasaki/

Brazil - World Nuclear Outlook Report - World Nuclear Association. (n.d.). https://world-nuclear.org/our-association/publications/world-nuclear-outlook-report/brazil---world-nuclear-outlook-report

Central Office, NucNet a.s.b.l., Brussels, Belgium. (2025, August 21). Sweden to restart uranium mining as government prepares for new reactors. The Independent Global Nuclear News Agency. https://www.nucnet.org/news/sweden-to-restart-uranium-mining-as-government-prepares-for-new-reactors-8-4-2025

Commission of the European Communities. (2026). Report on the implementation of the Euratom Treaty. [COM(2026)120]. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=COM:2026:120:FIN

Czerep, J. (2025, August 22). States Joining Queue for Niger's Uranium Deposits. Polish Institute of International Affairs.

Digges, C. (2025, January 9). This German town could decide the future of EU reliance on Russian nuclear fuel. Bellona.org. https://bellona.org/news/nuclear-issues/2025-01-this-german-town-could-decide-the-future-of-eu-reliance-on-russian-nuclear-fuel

Dyer, J. (2026, February 23). Serbia plans to build its first nuclear power plant by 2040. SightLine | U308. https://sightlineu3o8.com/2026/02/serbia-plans-to-build-its-first-nuclear-power-plant-by-2040/

Euratom Supply Agency. (2022). HALEU report: May 2022. https://euratom-supply.ec.europa.eu/system/files/2022-08/HALEU%20report%20May%202022%20print.pdf

Euratom Supply Agency. (2025). Euratom Supply Agency annual report 2024 : corrected edition, September 2025. Publications Office of the European Union. https://data.europa.eu/doi/10.2833/1837522.

European Commission. (2023). Net-Zero Industry Act. https://commission.europa.eu/topics/competitiveness/green-deal-industrial-plan/net-zero-industry-act_en

European Commission. (n.d.). Euratom Supply Agency: Annual reports. https://euratom-supply.ec.europa.eu/publications/esa-annual-reports_en

European Commission. (n.d.). Market Observatory. Euratom Supply Agency. https://euratom-supply.ec.europa.eu/activities/market-observatory_en

European Parliament. (2023). European Parliament resolution on small modular reactors. [TA-9-2023-0456]. https://www.europarl.europa.eu/doceo/document/TA-9-2023-0456_EN.html

European Parliament. (2023). Small modular reactors (SMRs). [Briefing]. https://www.europarl.europa.eu/thinktank/en/document/EPRS_BRI(2023)751456

European Parliament. (2024). Euratom: History and current challenges. [Briefing]. https://www.europarl.europa.eu/RegData/etudes/BRIE/2024/757796/EPRS_BRI%282024%29757796_EN.pdf

European Union. (1957). Treaty establishing the European Atomic Energy Community (Euratom). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=LEGISSUM%3A5050619

European Union. (2008). Consolidated version of the Treaty on the Functioning of the European Union - Article 194. https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX%3A12008E194%3AEN%3AHTML

European Union. (2014). Council Directive 2014/87/Euratom on nuclear safety. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32014L0087

European Union. (2024). Regulation (EU) 2024/1735 (Net-Zero Industry Act). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32024R1735

Ewokor, C. Armstrong, K. (2024, April 12). Russian troops arrive in Niger as military agreement begins. BBC. https://www.bbc.com/news/world-africa-68796359

International Atomic Energy Agency. (2007). Nuclear fuel cycle simulation system (VISTA). https://inis.iaea.org/records/tfb1f-3g053

Last uranium mine in Central Europe ceases operations after 60 years. (2021, April 8). Radio Prague International. https://english.radio.cz/last-uranium-mine-central-europe-ceases-operations-after-60-years-8194362

Lehner, J., & Camut, N. (2025, December 22). France enlists Russian state-owned company to help make nuclear fuel in Germany. POLITICO. https://www.politico.eu/article/france-russian-state-owned-nuclear-germany-fuel/

Lorenz, P. (2022, May 4 (2025)) Russian Grip on EU Nuclear Power. Wiener Umweltanwaltschaft

Lory, G. (2025, May 27). Why nuclear energy is making a comeback across Europe. Euronews. https://www.euronews.com/my-europe/2025/05/27/why-nuclear-energy-is-making-a-comeback-across-europe

Market Observatory. (n.d.). Supply Agency of the European Atomic Energy Community. https://euratom-supply.ec.europa.eu/activities/market-observatory_en

Mas, L. Roger, B. (2026, January 16). How a uranium supply coveted by Russia ended up in limbo in Niger. Le Monde.

Melly, P. (2025, August 27). Niger’s nuclear ambitions: Russia outsmarts France in Niger over proposed power plant. BBC. https://www.bbc.com/news/articles/c5y23lvm05no

Natulya, P. (2025, June 30). The Limits to China’s Transactional Diplomacy in Africa. Africa Center. https://africacenter.org/spotlight/china-transactional-diplomacy-africa-niger/

Niger–Uranium: Russian vessel off Lomé, stalled Yellowcake convoy, and the emerging risk of an airlift scenario | African Security Analysis. (n.d.). https://www.africansecurityanalysis.org/updates/niger-uranium-russian-vessel-off-lome-stalled-yellowcake-convoy-and-the-emerging-risk-of-an-airlift-scenario

Norman, W. (2025, March 18). Poland accelerates plans for its first nuclear power plant, report says. EuropaProperty.com. https://europaproperty.com/poland-accelerates-plans-for-its-first-nuclear-power-plant-report-says/

Nuclear Energy Diplomacy: Can the World Catch Up with Russia? (2026, January 18). World Nuclear Industry Status Report. https://www.worldnuclearreport.org/Nuclear-energy-diplomacy-Can-the-world-catch-up-with-Russia

Nuclear power plant. (n.d.). Riigiplaneering. https://riigiplaneering.ee/en/tuumajaam

Publications Office of the EU. (n.d.). General report on the activities of the European Union. https://op.europa.eu/en/publication-detail/-/publication/9f9b49e7-a7ec-11f0-a7c5-01aa75ed71a1/language-en

Russia’s nuclear energy diplomacy in the Middle East: why the EU should take notice. (n.d.). https://www.epc.eu/publication/Russias-nuclear-energy-diplom-2093d8/

Schneider, M. (2025). World nuclear industry status report 2025. https://www.worldnuclearreport.org/All-the-figures-from-the-2025-report

Siddi, M. Silvan, K. (2023, October). Russia and Kazakhstan in the global nuclear sector: From uranium mining to energy diplomacy. Finnish Institute of International Affairs. https://fiia.fi/en/publication/russia-and-kazakhstan-in-the-global-nuclear-sector

Szulecki, K., & Overland, I. (2023). Russian nuclear energy diplomacy and its implications for energy security in the context of the war in Ukraine. Nature Energy, 8(4), 413–421. https://doi.org/10.1038/s41560-023-01228-5

The Chinese-owned group Somina plans to resume uranium mining at Azelik (Niger). (2024, May 15). Enerdata. https://www.enerdata.net/publications/daily-energy-news/uranium-mining-restarting-production.html

The EU is dependent on Russian nuclear fuel – but not for long. (2025, November). The Hague Research Institute. https://hagueresearch.org/the-eu-is-dependent-on-russian-nuclear-fuel-but-not-for-long/

The Insider. (2022, November 10). Weaponized Rosatom: How Russia uses its nuclear plants abroad for blackmail and political pressure. https://theins.ru/en/economics/256858

Uranium in Kyrgyzstan - World Nuclear Association. (n.d.). https://world-nuclear.org/information-library/country-profiles/countries-g-n/kyrgyzstan

Uranium recovery starts at Finnish mine. (2024, June 19). World Nuclear News. https://www.world-nuclear-news.org/Articles/Uranium-recovery-starts-at-Finnish-mine

Westinghouse Electric Company. (2023). Westinghouse-led project will secure VVER fuel supply. https://info.westinghousenuclear.com/news/westinghouse-led-project-will-secure-vver-fuel-supply-in-europe-and-ukraine

Wiener Umweltanwaltschaft. (2012). https://wua-wien.at/images/stories/publikationen/uranium-mining.pdf

WISE Uranium Project. (n.d.). Issues at operating uranium mines and mills - Europe. https://www.wise-uranium.org/umopeur.html

Woodall, T. (2025, December 12). Explainer: Why Russia’s nuclear industry has escaped major sanctions. The Kyiv Independent. https://kyivindependent.com/explainer-why-russias-nuclear-industry-has-escaped-major-sanctions/

World Nuclear Association. (n.d.-a). Nuclear power in Belgium. https://world-nuclear.org/information-library/country-profiles/countries-a-f/belgium

World Nuclear Association. (n.d.-b). Nuclear power in Bulgaria. https://world-nuclear.org/information-library/country-profiles/countries-a-f/bulgaria

World Nuclear Association. (n.d.-c). Nuclear power in Czech Republic. https://world-nuclear.org/information-library/country-profiles/countries-a-f/czech-republic

World Nuclear Association. (n.d.-d). Nuclear power in Finland. https://world-nuclear.org/information-library/country-profiles/countries-a-f/finland

World Nuclear Association. (n.d.-e). Nuclear power in France. https://world-nuclear.org/information-library/country-profiles/countries-a-f/france

World Nuclear Association. (n.d.-f). Nuclear power in Germany. https://world-nuclear.org/information-library/country-profiles/countries-g-n/germany

World Nuclear Association. (n.d.-g). Nuclear power in Hungary. https://world-nuclear.org/information-library/country-profiles/countries-g-n/hungary

World Nuclear Association. (n.d.-h). Nuclear power in Italy. https://world-nuclear.org/information-library/country-profiles/countries-g-n/italy

World Nuclear Association. (n.d.-i). Nuclear power in Lithuania. https://world-nuclear.org/information-library/country-profiles/countries-g-n/lithuania

World Nuclear Association. (n.d.-j). Nuclear power in Netherlands. https://world-nuclear.org/information-library/country-profiles/countries-g-n/netherlands

World Nuclear Association. (n.d.-k). Nuclear power in Poland. https://world-nuclear.org/information-library/country-profiles/countries-o-s/poland

World Nuclear Association. (n.d.-l). Nuclear power in Romania. https://world-nuclear.org/information-library/country-profiles/countries-o-s/romania

World Nuclear Association. (n.d.-m). Nuclear power in Slovakia. https://world-nuclear.org/information-library/country-profiles/countries-o-s/slovakia

World Nuclear Association. (n.d.-n). Nuclear power in Slovenia. https://world-nuclear.org/information-library/country-profiles/countries-o-s/slovenia

World Nuclear Association. (n.d.-o). Nuclear power in Spain. https://world-nuclear.org/information-library/country-profiles/countries-o-s/spain

World Nuclear Association. (n.d.-p). Nuclear power in Sweden. https://world-nuclear.org/information-library/country-profiles/countries-o-s/sweden

World Nuclear Association. (n.d.-q). The European Union. https://world-nuclear.org/information-library/country-profiles/others/european-union

World Nuclear Association. (n.d.-r). High-assay low-enriched uranium (HALEU). https://world-nuclear.org/information-library/nuclear-fuel-cycle/conversion-enrichment-and-fabrication/high-assay-low-enriched-uranium-haleu

World Nuclear Association. (n.d.-s). Nuclear fuel cycle overview. https://world-nuclear.org/information-library/nuclear-fuel-cycle/introduction/nuclear-fuel-cycle-overview

World Uranium Mining Production - World Nuclear Association. (n.d.). https://world-nuclear.org/information-library/nuclear-fuel-cycle/mining-of-uranium/world-uranium-mining-production

Zaniewicz, M. (2023, September 5). Anatomy of Dependence: How to Eliminate Rosatom from Europe. Forum Energii. https://www.forum-energii.eu/en/anatomia-zaleznosci-rosatom

Comments